23 April 2015 3 menit

[The Jakarta Post] Analysis: Plantations under pressure

Kristiadi, Bahana, Jakarta | Business | Thu, April 23 2015, 8:07 AM

Soybean oil and palm oil are naturally interchangeable goods, translating to strong correlation in prices between the two commodities. Due to the abundance of global soybean oil, it is currently trading at its lowest price in five years, resulting in a narrowing of the crude palm oil (CPO) discount to soybean price (table 1). Factoring in these conditions, we maintain our bearish view on CPO prices in 2015.

The B15 program in the government’s diesel plan was launched this month, much sooner than September, as was previously scheduled. Hypothetically, with the implementation of B15, biodiesel consumption could jump 50 percent year-on-year (yoy) to 5.3 million kiloliters (kl) per annum, which would require feedstock of 4.7 to 5.3 million tons of CPO or 10 percent of Indonesia’s total CPO production, suggesting potential support for CPO prices going forward.

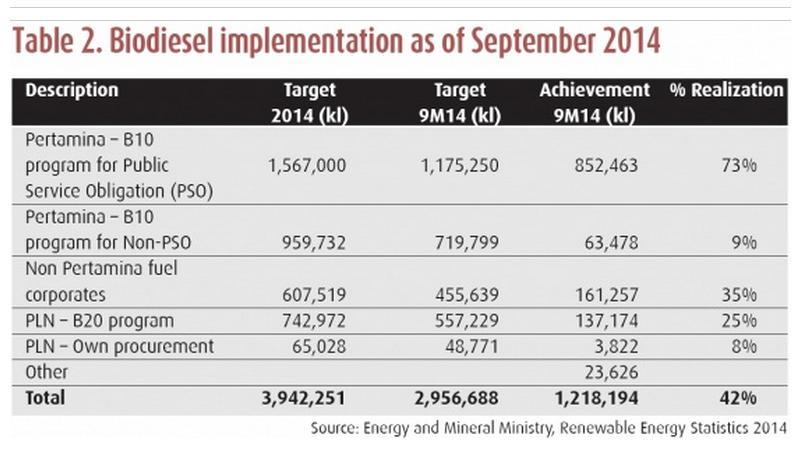

However, we believe two main issues from this biodiesel program remain unresolved: (1) lack of infrastructure to effectively distribute the biodiesel on a nationwide basis, and (2) weak enforcement and control from the government to ensure the achievement of blending targets. A look at the first nine months of 2014 (9M14) shows that realization levels were quite disappointing, with only a 42 percent consumption target achieved (table 2).

Meanwhile, low oil prices have reduced the feasibility of the biodiesel program. To solve the price mismatch, the government plans to launch a CPO-supporting fund program in the near future. The program will apply levies of US$50 per ton on CPO exports and $30 per ton on CPO-derivative products. The fund will then be used to cover the price differential from biodiesel blending and other activities in the CPO industry, for example replanting and R&D.

Although the government decree regarding the program has yet to be released, we see this move translating to Indonesian planters losing competitiveness against their Malaysian peers.

At this stage of the market cycle, we have lowered our CPO price assumption by 8 percent, from $725 per ton to $665 per ton (Rotterdam CIF) in 2015 on the back of weak commodity prices, sluggish global demand and policy risk. We note that the year-to-date (ytd) CPO price has averaged $672 per ton (2014 average: $815 per ton), down 18 percent yoy over the same period. Signs of weaker global demand can be seen in major CPO-importing countries such as India and China.

In summary, we maintain our underweight rating on the Indonesian plantation sector, and expect the sector’s ytd market underperformance to persist in the future.

_____________________

The writer is an analyst in the research department of Bahana Securities.

Link:

http://www.thejakartapost.com/news/2015/04/23/analysis-plantations-under-pressure.html